How is AI Voice being adopted across enterprises today? We draw on case studies, adoption data and customer insights to show where traction is strongest and how usage is evolving. This is an extract from CPaaSAA’s report AI Voice: Who Will Run The Conversation? – you can download the full report here.

Adoption is growing fast, but uneven

There is clear evidence of rapid deployment across enterprise environments, particularly in service-intensive sectors. However, adoption remains uneven and early-stage.

The report highlights that meaningful deployment is visible in larger service organisations, but overall maturity is still developing. In many cases, usage is estimated to be well below 10% of its potential, with most implementations focused on initial use cases rather than full-scale transformation.

Headline insight: AI Voice adoption is accelerating, but is initially concentrated in early-stage, high-impact use cases.

The adoption pattern illustrated in the report shows a staged progression: organisations first make conversations computable, then automate routine interactions, and eventually move towards autonomous AI Voice systems.

This matters because adoption is typically not a single step. It reflects a sequence of capability building, where each stage increases both value and complexity.

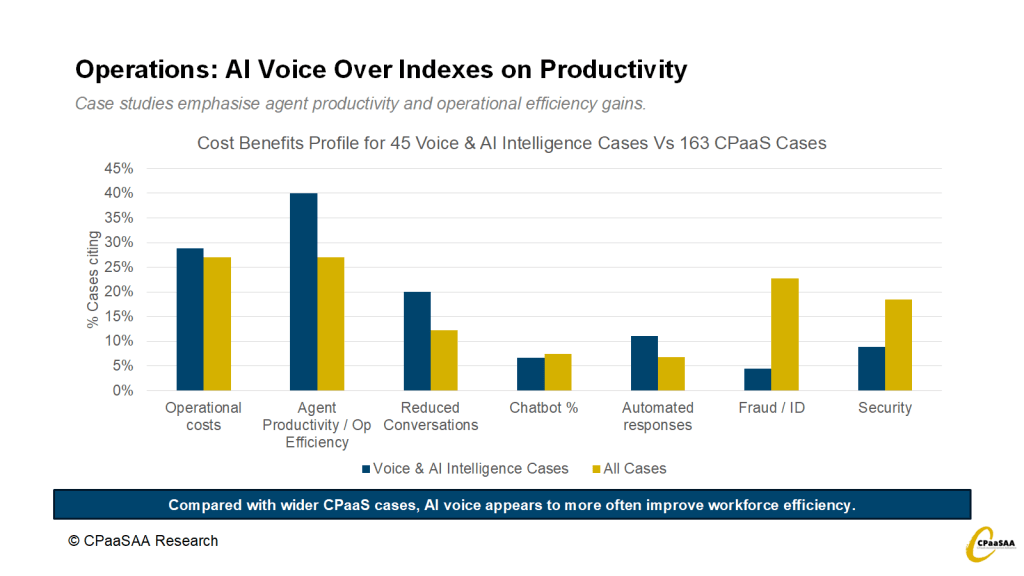

What is driving adoption today

The report identifies a clear set of demand drivers from enterprise buyers.

- The primary driver is managing increasing volumes of customer interaction and the inefficiencies this exposes

- Customer experience improvement follows closely

- Cost reduction is important, but often a secondary outcome

- In regulated sectors, security and compliance are leading priorities

Survey data reinforces this:

- 33% contact reduction

- 32% customer satisfaction

- 22% cost reduction

(Source: CPaaSAA Case Directory analysis; Contact Center Helper survey 2025)

This reflects a shift in buying logic. As noted by industry contributors, organisations are increasingly focused on scaling interaction without linear increases in cost.

The chart highlights how demand clusters around volume handling, service quality and efficiency.

Where adoption is strongest

Adoption varies significantly by sector and organisational type.

- High voice-usage sectors such as telecoms, financial services and healthcare are leading

- Regulated industries are early adopters due to compliance needs

- Digital-native organisations move faster than traditional enterprises

Call centres are a focal point. More than 60% of organisations are prioritising automation and assistance in the near term, with analytics close behind (Contact Center Helper, 2025)

Adoption is shaped by capability and complexity

Adoption is not only demand-driven. Supply-side complexity also shapes progression.

Most enterprises begin with transcription and summarisation, which provide the structured data foundation for more advanced use cases. From there, organisations expand into triage, dialogue and automation.

This staged progression reflects both technical feasibility and organisational readiness.

Stakeholder implications

For CPaaS and Intelligent Engagement players:

- Early-stage adoption creates entry points through efficiency tools

- Long-term value depends on automation and orchestration

For enterprises:

- The priority is moving from isolated deployments to integrated workflows

What’s next?

This article has focused on how AI Voice is being adopted today and the drivers behind that adoption.

The next article will examine market size, growth and forecasts, and what they imply for the trajectory of AI Voice.

You can download the full report here.

Andrew Collinson

Andrew Collinson is a telecoms and connected technologies expert, specializing in growth strategy, research, and thought leadership. As founder of Connective Insights, he helps clients translate new technologies into viable business models, with a focus on CPaaS, APIs, platform strategies, AI, and network automation.

Before joining CPaaSAA as Associate Research Partner, Andrew was Research and Commercial Director at STL Partners for 15 years, leading a successful research business. He also moderates events, conducts bespoke research, and advises on telecom innovation, stakeholder dynamics, and digital transformation.

Comments are closed